The platform’s administration heavily promotes its repertoire of recurring promotional campaigns and trading competitions. Rhetoric regarding the structural advantages of Contracts for Difference (CFDs), the availability of comprehensive educational suites, and access to expert advisory services remains a focal point of their marketing. However, despite this polished veneer, reality dictates that the intermediary operates under the sole regulatory purview of an offshore commission, automatically binding its legal registration to an offshore jurisdiction. Predictably, public sentiment aligns with this configuration; independent client testimonials remain overwhelmingly critical, with the remaining positive commentary bearing the hallmarks of manufactured astroturfing. In this analytical Prorex Limited review, we will examine whether the entity can be classified as a fraudulent enterprise.

About Our Team

Prorex Limited Snapshot

| Claimed Regulation | MFSC |

| Verified Regulation | MFSC |

| Licence Last Checked | 20/05/2026 |

| Minimum Deposit | $100 |

| Retail Leverage up To | 1:200 |

| Affiliate Programme | Up to $10 per Lot |

| Type of Education | FAQ |

| Claimed Year Foundation | 2024 |

| Domain Parked Since | 28/08/2024 |

| Trading Software | MetaTrader 5 |

| Mobile Compatibility | iOS, Android |

| Languages Supported | En, Ja |

Advantages and Disadvantages

-

A dedicated frequently asked questions (FAQ) module is readily accessible.

-

Regulatory oversight is confined to an offshore commission.

-

Operational emphasis is disproportionately placed on inherently volatile CFDs.

-

Potential manipulation risks associated with the trading terminal.

-

High, financially hazardous leverage structures.

-

Preponderance of adverse or commercially procured client testimonials.

Legitimacy Check

The fundamental legitimacy of the prorexglobal.com website is of paramount importance, given its profound implications for the structural integrity of the broker-trader dynamic. We decided to dissect the regulatory framework governing this entity with rigorous scrutiny. Furthermore, a thorough examination of its corporate registration, headquarters, market longevity, and the realistic prospects of capital recovery in the event of a contractual dispute is essential.

To begin with, the operational architecture of Prorex Limited is nominally monitored by the regulatory body of Mauritius. While verifying this credential via the official registry of the regulator is a simple matter, the practical efficacy of such a weak regulatory framework is highly questionable. Such relaxed oversight invariably introduces significant headwinds for retail participants, often culminating in highly contentious scenarios. For instance, we wonder whether clients fully appreciate that there remains an inherently high probability of arbitrary account suspension, coupled with an equally pervasive risk of withdrawal denials. Moreover, non-aligned brokerages frequently engage in pricing distortions by exploiting backend controls on the trading terminal.

The corporate registration of Prorex Limited mirrors its regulatory status, being firmly anchored within an offshore jurisdiction. The possession of a licence from the Mauritius Financial Services Commission (FSC) logically confirms that the corporate entity is domiciled there. This offshore corporate configuration introduces a litany of structural risks. Firstly, such entities do not participate in statutory investor compensation funds, meaning that in the event of an insolvency, retail capital recovery is non-existent. Secondly, the potential commingling of client deposits with corporate operational capital remains a persistent risk — an absolute red flag for institutional and retail participants alike. A further operational bottleneck pertains to payment gateways, as Tier-1 European banking institutions routinely decline transactional clearing with offshore entities. Consequently, the broker is compelled to route capital through opaque, informal payment channels, which inevitably inflates transaction fees.

Furthermore, the contact repository on the prorexglobal.com domain lists a registered corporate address within Mauritius. However, cross-referencing these coordinates via geospatial mapping tools fails to confirm the presence of any physical corporate infrastructure. This absence is compounded by a pervasive veil of corporate anonymity; verifiable disclosures regarding executive leadership or ultimate beneficial owners are entirely absent. Such opacity is characteristic of fringe brokerages operating with substandard institutional trust and a compromised reputation within the wider trading community.

The operational lifespan of Prorex Limited can be calculated by cross-referencing its licensing date with domain registration metrics. The former indicates an inception year of 2024, a timeline corroborated by a rudimentary WHOIS search and WebArchive data. Thus, the subject of this review has been active in the marketplace only since 2024. This brief track record represents a distinct disadvantage, reflected in negligible brand equity and a scarce volume of organic consumer feedback.

Prorexglobal.com Content Quality

The digital portal of Prorex Limited exhibits several functional and structural deficiencies that require careful examination. Below, we will evaluate the onboarding protocols, the user interface architecture, and the availability of mandatory legal documentation.

In assessing the critical vulnerabilities of the portal, the most immediate cause for concern is the instability of the site’s SSL security architecture, which severely compromises data privacy. Indeed, across most standard web browsers, security protocols prevent the homepage from loading entirely. A secondary issue stems from a lack of transparency; the core parameters governing the trading partnership are systematically obscured from the user. Furthermore, poor platform optimisation results in visual rendering anomalies across desktop and mobile devices, alongside protracted page latency.

Overall, the site suffers from numerous errors, glitches, and imperfections. The About section contains a completely absurd statement about 10,284 countries where the broker is present and the same number of regulators. The platform lacks a live-chat utility for real-time support, and there are no links to verified corporate social media profiles — a significant omission in modern digital brokerages. The absence of utility plugins and responsive mobile optimisation further degrades the user experience. Even the account tier matrix, where transparent trading costs should be disclosed, is heavily restricted.

Crucially, the digital registration funnel was entirely non-functional at the time of writing, returning a standard “404 Error” page. This operational anomaly points toward predatory onboarding practices; the administration effectively forces prospective traders into direct, unmonitored communication with account managers. Furthermore, independent reviews of the internal client dashboard indicate a rudimentary functional framework, limited to basic profile editing and unverified deposit/withdrawal modules.

Key Trading Features

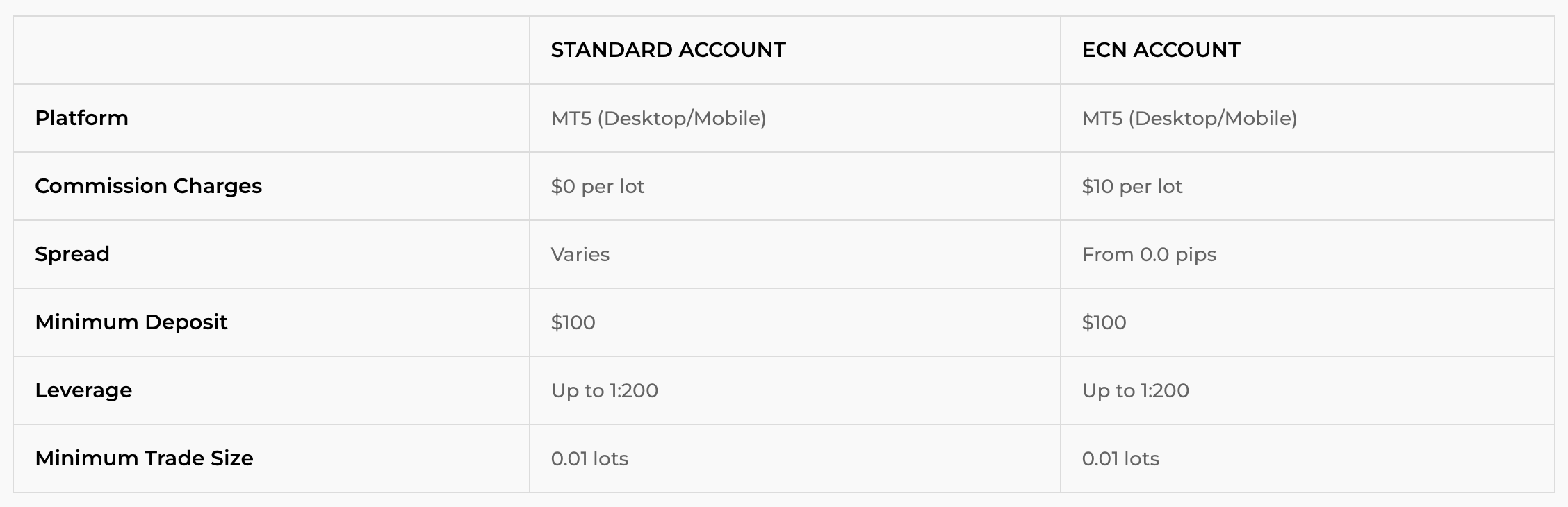

Prorex Limited provides a highly restricted selection of account types, nominally categorised into Standard and ECN tiers. The differentiation between these tiers relies on floating commission structures and variable spreads. We wonder how the platform justifies its lack of asset transparency, given that the underlying catalogue of financial instruments is not explicitly disclosed.

In practice, available assets at Prorex Limited are highly restricted and subject to arbitrary modification. Furthermore, the platform’s exclusive focus on CFDs creates an environment where retail loss ratios regularly exceed the 80% threshold. The absence of standard regulatory risk disclosures regarding CFDs further deviates from the compliance benchmarks maintained by reputable, tier-1 licensed brokerages.

The minimum deposit requirement is set at a flat entry point of $100 across all account tiers. While an adjustable deposit threshold is common among unaligned entities to capture varying levels of retail capital, we decided to caution against capital allocation here, irrespective of any promised premium services. This caution is reinforced by Prorex Limited heavy reliance on cryptocurrency as the primary mechanism for financial settlement — a classic hallmark of high-risk corporate structures.

The leverage limit extends to 1:200. While this falls within permissive offshore regulatory boundaries, it stands in stark contrast to the strict leverage caps mandated by European authorities to protect retail capital. The combination of complex CFD instruments and high leverage increases the speed at which retail accounts can face total capital depletion.

Supplementary services at Prorex Limited remain basic, limited to a static FAQ module rather than responsive client support. The referral framework operates on an Introducing Broker (IB) model, promising returns of up to $10 per lot on referred volume. However, these promotional claims should be viewed with considerable scepticism.

Prorex Limited Custom Utilities Insight

The account documentation states that the platform utilises the MetaTrader 5 engine. However, the use of this software does not automatically guarantee fair execution or optimal transaction speeds. The platform administration maintains full sovereignty over the internal server configuration, allowing them to adjust spreads, introduce execution latency, and alter price feeds at their discretion. Consequently, the terminal remains vulnerable to internal manipulation designed to erode client balances over time.

Customer Service Overview

Corporate communication with Prorex Limited is restricted to a single point of contact via electronic mail. Independent validation of the corporate mail server suggests that standard helpdesk inquiries face significant security and delivery risks. Alternative communication channels, such as live chat, telephone support, or official social media integration, are entirely absent.

Our Verdict

We have decided to explicitly advise against engaging with Prorex Limited. The intermediary operates under weak regulatory oversight and is registered in an offshore jurisdiction. The project faces widespread consumer criticism, structural account registration failures, and disadvantageous trading conditions — notably excessive leverage ratios and high commission overheads.

About the author

My professional experience indicates that this entity exhibits the standard characteristics of a fraudulent brokerage. The digital infrastructure lacks basic SSL security protocols, and the mandatory settlement of balances via cryptographic assets serves as a clear warning sign. I cannot recommend this platform.